The Balance Sheet

As everyone knows, the Fed's balance sheet has more than tripled since the financial crisis. Here is a look at the liability side of the Fed's balance sheet:

What's interesting here is that prior to the crisis, almost all the Fed's liabilities were in the form of (zero-interest) cash -- that is, currency in circulation (the blue area). No one knows for sure, but probably over half of this cash is circulating outside the U.S.

At the time of the financial crisis, the balance sheet doubled over a very short period of time, and has continued to grow since then. What's interesting here is that subsequent to the crisis, most of the growing liabilities are in the form of interest-bearing reserves (held by depository institutions with accounts at the Fed).

Now, three trillion dollars sounds like a heck of a lot of liabilities. There is no danger of bankruptcy, however. That's because Fed liabilities are not debt; or, if they are (as in the case of reserves), they are made redeemable in cash, which the Fed can print at any time. Fed liabilities are more like equity shares, than debt. That is, there is a risk of dilution (inflation), but no risk of bankruptcy.

Next question: what did the Fed do with all this money it "printed" up (out of thin air, I might add)? Many people are likely to conjure up an image of "Helicopter Ben."

Next question: what did the Fed do with all this money it "printed" up (out of thin air, I might add)? Many people are likely to conjure up an image of "Helicopter Ben."

Alas, that's not quite how it works (even if it does work this way in some other countries, like the recent experience in Zimbabwe). You see, while the Fed is "pumping money into the economy," it is simultaneously sucking some other group of assets out of the economy.

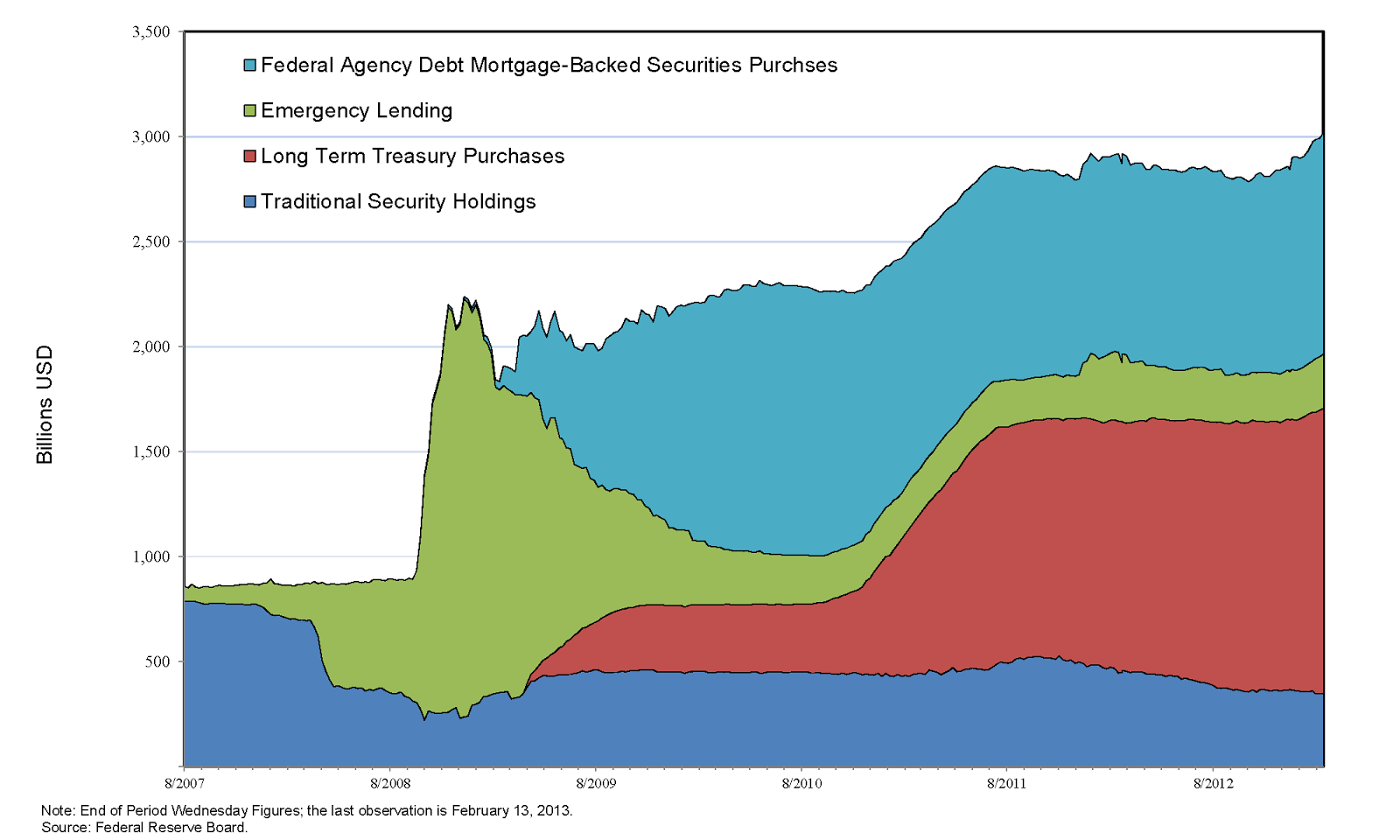

To put things in a slightly different way, the Fed is acting much like, um...well, much like a bank. That is, the Fed finances acquisitions of less liquid assets with more liquid liabilities. The Fed's liquid liabilities look a lot like super short duration Treasuries. What do the assets look like? Take a look here:

Most of the assets consist of interest-bearing securities, primarily U.S. government debt and agency MBS. In 2012, this portfolio yielded over 3%. In 2012, the Fed remitted $89B to the Treasury (historically, remittances have been around $25B per year). Not a bad return, for a year of "helicopter drops."

In the meantime, inflation appears to be fairly well centered around the Fed's 2% inflation target (recent data is coming in below target):

TIPS based measures of inflation expectations appear to be fairly well centered around 2% as well (recent data appears to be rising a bit away from target):

While inflation and inflation expectations appear to be muted for the time-being, a number of economists and Fed officials still worry about the various risks associated with the Fed's large and growing balance sheet. The most obvious worry is the risk of inflation. The extent to which one worries about inflation depends a lot on one's theory of inflation, which I will explain below.

(New) Keynesian View

In the extreme version of this view (Woodford's cashless economy), Fed liabilities serve only as a unit of account; and the private sector manufactures the "money" it needs. The Fed determines (influences) the nominal interest rate, which influences the aggregate demand (AD) for goods and services. Inflation is determined in part by the pricing decisions of firms. When AD is strong, prices rise more rapidly; and conversely when AD is weak. Inflation is also determined in part by the Fed's policy function (Taylor rule), which stipulates a long-term inflation target (serving as the nominal anchor) together with the promise to alter the interest rate (hence AD) in response to undesirable movements in inflation away from target.

Conspicuously absent from the theory of inflation above is any role played by the money supply. The Fed's balance sheet plays no role in determining inflation according to this view. It follows as a corollary that the size of the Fed's balance sheet poses no economic risk.

This world view likely explains the statements made by the more dovish members of the FOMC. Inflation is low because aggregate demand is weak. We need to keep interest rates low. Additional QE by the Fed is mostly innocuous--except possibly for political reasons. What do I mean by this? Let me explain.

Federal Reserve Board economist Seth Carpenter (and his coauthors) have recently distributed an interesting working paper that offers a methodology for making projections about the way the Fed's balance sheet is to evolve over time, see: The Federal Reserve's Balance Sheet: A Primer and Projections. In some of their projections, the Fed actually incurs an operating loss and remittances to the U.S. Treasury cease for a while. The economic consequences of this are innocuous if you're coming at things from a strict New Keynesian perspective. But the optics can be made to look bad, something that politicians hostile to the Fed are likely to exploit. Let me consider a simple example.

The Fed currently pays 1/4% on excess reserves, which are presently close to $2T. In one year's time, and under currently policy, reserves will be closer to $3T. The annual interest expense associated with these reserve liabilities is presented in the following table, for various interest rates (IOR):

Now, perhaps this is unlikely, but it is certainly not outside the realm of possibility: Imagine that inflation and inflation expectations begin to rise sharply at the end of 2013. The Fed's policy response is to jack up it's policy rate (IOR) sharply, say, to 3%. If reserves remain close to $3T, that's about $90B in interest payments to banks and hence, $90B less in remittances to the Treasury.

From an economic (a consolidated Fed and Treasury balance sheet) perspective, interest-bearing reserves look a lot like interest-bearing Treasuries. So whether the Fed or the Treasury services this debt makes little difference to the American taxpayer. Naturally, this is not the way things will be portrayed in the political arena.

(New) Monetarist View

According to this view, there are financial market imperfections (limited commitment, asymmetric information, etc.) that allow Fed and Treasury liabilities to be valued for their liquidity/collateral properties. Inflation, in the long-run at least, is determined by the supply and demand for currency (a special type of Fed liability).

In normal times, currency is dominated in rate of return, so their is a well-defined demand for the stuff. As well, in normal times, reserves are dominated in rate of return, so Fed liabilities are mostly in the form of currency (see first diagram above, prior to 2008). A well-defined demand for currency plus Fed control over the supply of currency means that the Fed can control inflation.

In abnormal times, however, reserves and Treasuries earn (roughly) the same rate of return. In this case, the Fed only controls the total supply of its liabilities--the composition of these liabilities between currency and reserves is determined by banks. Reserves are like a demand deposit liability--convertible into currency on demand. The Fed can influence bank redemption policies by manipulating IOER--if it has this tool available. Note that the Fed has only had this tool available since 2008. (And in light of the political risks outlined above, one could easily imagine Congress taking this tool away.)

If inflation and inflation expectations begin to rise, so should the nominal demand for currency (even if the real demand remains more or less fixed). One might expect a flood of currency into the economy as banks exercise their redemption option on reserves. The flood of currency could potentially validate the higher inflation expectations -- a self-fulfilling prophesy.

[Note: I have refined this idea in this post here: Excess Reserves and Inflation Risk (June 22, 2014) ]

In many of our models, we assume passive support from the Treasury to support whatever needs to be done to keep inflation in check. But how realistic is this? What if that support does not materialize? And moreover, suppose that the Fed is no longer permitted to use IOR as a policy tool? What if inflation and inflation expectations start to rise? What then?

In this case, the only way the Fed can "suck out" excess liquidity is via asset sales. In a sense, the value of the Fed's assets represents the extent to which the Fed can credibly commit to withdraw cash from circulation (the Fed has no ability to tax). But if inflation expectations rise, so will longer term interest rates. The Fed's assets will decline in value. And with the decline in value, the ability to purchase cash.

What sort of capital losses are we talking here? Obviously, it depends. The average maturity of the Fed's asset portfolio is around 10 years (up significantly from historical norms, thanks to Operation Twist, etc.). The following formula provides a rough approximation of exposure to interest rate risk:

1 ppt increase in the interest rate = (average duration)% decline in bond price

So, to take a bad (but not worse case) scenario, suppose interest rates rise by 5 ppt (e.g., China decides to unload its holdings of U.S. Treasuries?). We are talking about a 50% (somewhat less) loss on the Fed's $3T portfolio. The remaining $1.5T in asset value would not be enough to suck out the current $2T in reserves. There would be $0.5T in reserves remaining--representing $0.5T in potential new currency (a 50% increase over the current supply of $1T).

Conclusions

No one knows for sure which of the two theories of inflation above is the better approximation for our current reality. Central bankers are charged with the task of evaluating the risk of their policies under different theoretical scenarios. If the monetarist view is correct, then continued expansion of the Fed's balance sheet exposes the economy to ever higher inflation risk. Of course, this is not to say that the risk is not worth taking. Policymakers just need to be aware of the risk and make provisions for it.

It is interesting to note, however, that independent of one's theory of inflation, the large and growing balance sheet may expose the Fed to a certain type of political risk. If tightening needs to happen in the future, the Fed will have to raise interest rates (IOR) and/or sell off its assets. IOR may be made to look like Fed Reserve (instead of Treasury) transfers to the banking sector, at taxpayer expense. Capital losses on asset sales would similarly reduce remittances to the Treasury. It's not going to look very pretty.

As everyone knows, the Fed's balance sheet has more than tripled since the financial crisis. Here is a look at the liability side of the Fed's balance sheet:

At the time of the financial crisis, the balance sheet doubled over a very short period of time, and has continued to grow since then. What's interesting here is that subsequent to the crisis, most of the growing liabilities are in the form of interest-bearing reserves (held by depository institutions with accounts at the Fed).

Now, three trillion dollars sounds like a heck of a lot of liabilities. There is no danger of bankruptcy, however. That's because Fed liabilities are not debt; or, if they are (as in the case of reserves), they are made redeemable in cash, which the Fed can print at any time. Fed liabilities are more like equity shares, than debt. That is, there is a risk of dilution (inflation), but no risk of bankruptcy.

Next question: what did the Fed do with all this money it "printed" up (out of thin air, I might add)? Many people are likely to conjure up an image of "Helicopter Ben."

Next question: what did the Fed do with all this money it "printed" up (out of thin air, I might add)? Many people are likely to conjure up an image of "Helicopter Ben." Alas, that's not quite how it works (even if it does work this way in some other countries, like the recent experience in Zimbabwe). You see, while the Fed is "pumping money into the economy," it is simultaneously sucking some other group of assets out of the economy.

To put things in a slightly different way, the Fed is acting much like, um...well, much like a bank. That is, the Fed finances acquisitions of less liquid assets with more liquid liabilities. The Fed's liquid liabilities look a lot like super short duration Treasuries. What do the assets look like? Take a look here:

In the meantime, inflation appears to be fairly well centered around the Fed's 2% inflation target (recent data is coming in below target):

While inflation and inflation expectations appear to be muted for the time-being, a number of economists and Fed officials still worry about the various risks associated with the Fed's large and growing balance sheet. The most obvious worry is the risk of inflation. The extent to which one worries about inflation depends a lot on one's theory of inflation, which I will explain below.

In the extreme version of this view (Woodford's cashless economy), Fed liabilities serve only as a unit of account; and the private sector manufactures the "money" it needs. The Fed determines (influences) the nominal interest rate, which influences the aggregate demand (AD) for goods and services. Inflation is determined in part by the pricing decisions of firms. When AD is strong, prices rise more rapidly; and conversely when AD is weak. Inflation is also determined in part by the Fed's policy function (Taylor rule), which stipulates a long-term inflation target (serving as the nominal anchor) together with the promise to alter the interest rate (hence AD) in response to undesirable movements in inflation away from target.

Conspicuously absent from the theory of inflation above is any role played by the money supply. The Fed's balance sheet plays no role in determining inflation according to this view. It follows as a corollary that the size of the Fed's balance sheet poses no economic risk.

This world view likely explains the statements made by the more dovish members of the FOMC. Inflation is low because aggregate demand is weak. We need to keep interest rates low. Additional QE by the Fed is mostly innocuous--except possibly for political reasons. What do I mean by this? Let me explain.

Federal Reserve Board economist Seth Carpenter (and his coauthors) have recently distributed an interesting working paper that offers a methodology for making projections about the way the Fed's balance sheet is to evolve over time, see: The Federal Reserve's Balance Sheet: A Primer and Projections. In some of their projections, the Fed actually incurs an operating loss and remittances to the U.S. Treasury cease for a while. The economic consequences of this are innocuous if you're coming at things from a strict New Keynesian perspective. But the optics can be made to look bad, something that politicians hostile to the Fed are likely to exploit. Let me consider a simple example.

The Fed currently pays 1/4% on excess reserves, which are presently close to $2T. In one year's time, and under currently policy, reserves will be closer to $3T. The annual interest expense associated with these reserve liabilities is presented in the following table, for various interest rates (IOR):

(New) Monetarist View

According to this view, there are financial market imperfections (limited commitment, asymmetric information, etc.) that allow Fed and Treasury liabilities to be valued for their liquidity/collateral properties. Inflation, in the long-run at least, is determined by the supply and demand for currency (a special type of Fed liability).

In normal times, currency is dominated in rate of return, so their is a well-defined demand for the stuff. As well, in normal times, reserves are dominated in rate of return, so Fed liabilities are mostly in the form of currency (see first diagram above, prior to 2008). A well-defined demand for currency plus Fed control over the supply of currency means that the Fed can control inflation.

In abnormal times, however, reserves and Treasuries earn (roughly) the same rate of return. In this case, the Fed only controls the total supply of its liabilities--the composition of these liabilities between currency and reserves is determined by banks. Reserves are like a demand deposit liability--convertible into currency on demand. The Fed can influence bank redemption policies by manipulating IOER--if it has this tool available. Note that the Fed has only had this tool available since 2008. (And in light of the political risks outlined above, one could easily imagine Congress taking this tool away.)

If inflation and inflation expectations begin to rise, so should the nominal demand for currency (even if the real demand remains more or less fixed). One might expect a flood of currency into the economy as banks exercise their redemption option on reserves. The flood of currency could potentially validate the higher inflation expectations -- a self-fulfilling prophesy.

[Note: I have refined this idea in this post here: Excess Reserves and Inflation Risk (June 22, 2014) ]

In many of our models, we assume passive support from the Treasury to support whatever needs to be done to keep inflation in check. But how realistic is this? What if that support does not materialize? And moreover, suppose that the Fed is no longer permitted to use IOR as a policy tool? What if inflation and inflation expectations start to rise? What then?

In this case, the only way the Fed can "suck out" excess liquidity is via asset sales. In a sense, the value of the Fed's assets represents the extent to which the Fed can credibly commit to withdraw cash from circulation (the Fed has no ability to tax). But if inflation expectations rise, so will longer term interest rates. The Fed's assets will decline in value. And with the decline in value, the ability to purchase cash.

What sort of capital losses are we talking here? Obviously, it depends. The average maturity of the Fed's asset portfolio is around 10 years (up significantly from historical norms, thanks to Operation Twist, etc.). The following formula provides a rough approximation of exposure to interest rate risk:

1 ppt increase in the interest rate = (average duration)% decline in bond price

So, to take a bad (but not worse case) scenario, suppose interest rates rise by 5 ppt (e.g., China decides to unload its holdings of U.S. Treasuries?). We are talking about a 50% (somewhat less) loss on the Fed's $3T portfolio. The remaining $1.5T in asset value would not be enough to suck out the current $2T in reserves. There would be $0.5T in reserves remaining--representing $0.5T in potential new currency (a 50% increase over the current supply of $1T).

Conclusions

No one knows for sure which of the two theories of inflation above is the better approximation for our current reality. Central bankers are charged with the task of evaluating the risk of their policies under different theoretical scenarios. If the monetarist view is correct, then continued expansion of the Fed's balance sheet exposes the economy to ever higher inflation risk. Of course, this is not to say that the risk is not worth taking. Policymakers just need to be aware of the risk and make provisions for it.

It is interesting to note, however, that independent of one's theory of inflation, the large and growing balance sheet may expose the Fed to a certain type of political risk. If tightening needs to happen in the future, the Fed will have to raise interest rates (IOR) and/or sell off its assets. IOR may be made to look like Fed Reserve (instead of Treasury) transfers to the banking sector, at taxpayer expense. Capital losses on asset sales would similarly reduce remittances to the Treasury. It's not going to look very pretty.

Good stuff, DA.

ReplyDeleteThank you! :)

Delete"In normal times, currency is dominated in rate of return, so their is a well-defined demand for the stuff."

ReplyDeleteCan you explain what you mean by that?

Sure thing, JP.

DeleteThink about a standard monetary model with a CIA constraint. By "normal" times, I meant a positive nominal interest rate, so that the CIA constraint binds tightly. When the CIA constraint is slack, individuals view zero-interest currency and zero-interest Treasuries as perfect substitutes, so that the demand for currency is indeterminate.

Ok, I think I see what you're saying. So the Fed can't influence inflation during abnormal times because the CIA constraint doesn't bind? The demand for currency is not "well-defined", so to say?

DeleteIf so, how would inflation ever begin to rise?

I like your points about the potential lack of Treasury support and the image of the Fed "sucking out" excess liquidity via asset sales, a difficult thing to accomplish if it doesn't have enough assets. I was writing a post on similar ideas and just put it up. Here.

http://jpkoning.blogspot.ca/2013/03/is-it-irrelevant-when-central-bank-goes.html

DeleteSo the Fed can't influence inflation during abnormal times because the CIA constraint doesn't bind? The demand for currency is not "well-defined", so to say?

DeleteIn the class of models I am thinking about, that is correct. What matters is the stock of total government liabilities, not their division between money and bonds (at the ZLB).

Just read your post. Yes, we are saying exactly the same thing except -- I make explicit that this is just one interpretation (monetarist). There is another influential theory (New Keynesian) that does not place such emphasis on the Fed's balance sheet.

"IOR may be made to look like Fed Reserve (instead of Treasury) transfers to the banking sector, at taxpayer expense."

ReplyDeleteIt really is a transfer if IOR > FF (negative seignorage).

Which is the case now.

Max, by FF do you mean the Federal Funds rate? In any case, I think the relevant rate of return differential would be the yield on assets held by the Fed (over 3% last year) minus the cost of funds (less than IOR, if you take into account the zero-interest liabilities issued by the Fed.

DeleteIf the yield on the most reserve-like bond (very short term treasuries) is <0.1% and IOR=0.25%, then the Fed is unambiguously losing money on seignorage.

DeleteGains (or losses) from interest rate speculation are irrelevant. Average funding cost isn't relevant either, only marginal cost, which is IOR.

0.2% * $2 trillion = $4 billion loss per year. Not a trivial amount I would say.

Max, how do you explain the $89B remitted back to the Treasury in 2012 then?

DeleteIsn't the point of economic analysis to look through the optics and understand the actual implications of certain actions?

ReplyDeleteThe Fed is a branch of government. If government default (and 8% rates can only happen if people begin to have a pretty high confidence in a Treasury default), doesn't it really matter that a branch of government is going to default (or let inflation soar) as well?

The federal government is a net debtor. How is it going to suffer from higher than expected inflation?

Plus on a 500 bp move, convexity on a 10yr bond is actually reasonably large...

Frankly I am not convinced that your negative scenario is negative at all...

The federal government is a net debtor. How is it going to suffer from higher than expected inflation?

DeleteThere is a short-term gain by implicit default through an unexpected inflation, but a long-term pain, as creditors will discount new debt issue more heavily.

David,

ReplyDeleteIn your New Monetarist view, pre-existing reserves seem irrelevant to the amount of currency. At any given FFR, the Fed will supply the banking system with as much currency as it demands -- supply is perfectly elastic.

If the above is correct, then interest-bearing reserves are just short duration liabilities of the government. That is, for any increase in the IOR, the cost flows through to Treasury. Thus, as the Fed does QE, it merely converts long duration Treasury liabilities to short duration ones. At the extreme case -- $8tr or so of QE -- Treasury would be effectively funding itself overnight.

Where reserves are relevant to money is that the Fed issues them to pay interest (absent a recapitalization) when it experiences a negative net interest margin. Unlike QE, this is a helicopter drop. It is not an asset swap, but a payment that raises bank profits.

If I have it right, then my question is, why continue to talk about reserves as "money" or the "monetary base". This confuses the issue, which is that 1) Treasury (taxpayer) duration risk is increasing dramatically; and 2) the Fed will conduct helicopter drops with a negative NIM.

Diego,

DeleteWhat you say sounds largely correct. But let me quibble.

If the Fed is conducting helicopter drops when NIM is negative, then it must be conducting "negative helicopter drops" when NIM is positive (as it is today). Is this how you want to think of it?

And yes, if NIM is negative, the Fed would basically just print money (credit reserve accounts) to meet its interest and dividend obligations. But whether this constitutes a helicopter drop depends on whether the monetary injection is permanent or not. In fact, the injection is recorded as a "deferred asset," which is paid down over time when NIM is expected to return to normal (positive). This is not inflationary in the NK world at all (since balance sheet does not matter), and also not inflationary in the NM world (if the operation is credibly transitory).

David,

DeleteIn the case of no recapitalization, the Fed makes a net payment of reserves to the private sector when it has a negative NIM. If there were a fiscal recap, that payment would be offset by a debit to Treasury's account.

Today, the Treasury makes a net payment to the Fed, and the Fed just credits Treasury's account with the proceeds. This is the equivalent of a "negative recapitalization".

Thus under the special case of no recapitalization, a negative NIM is a helidrop.

Regarding "permanence": if the Fed does not shrink its balance sheet, it could stay in a negative NIM position ad infinitum. That is, if inflation rises as a result of the NIM helidrop, the Fed will have to "chase" that acceleration with a higher IOR to prevent the real rate from falling. The only way out of this dynamic is to produce a positive real rate spike. However, this might plunge the economy into a '37-like "mini depression". The longer the Fed resists imposing a positive real rate, the more it will produce helidrops.

Another way of putting it: in theory, the NPV of seigniorage is always positive, and no NIM helidrop is expected to be permanent. In practice, there is path dependence and feedback loops occur.

DeleteDavid: I, too, have wondered about the political implications of an increase of IOR. Most of the public has little to no understanding of the Fed. And, somewhat surprisingly, most anti-Fed types (who care enough about the Fed to read books/websites/etc) don't seem to know that the Fed remits to the Treasury. (They dislike the Fed because they believe it is a cabal of private bankers benefiting at the expense of the American public.)

ReplyDeleteTo be outraged by increased IOR, as you suggest, it would seem that the broader public would first have to gain a basic understanding of how the Fed operates. Similarly, anti-Fed types would first have to be persuaded that they are wrong in normal times in order to be persuaded that they are "right" with respect to increasing IOR (scare quotes, since American public /= American taxpayer and the welfare consequences of increasing IOR may be positive). My guess is that both educational campaigns would be ineffective. A few, informed and otherwise normal folks would join the anti-Fed movement (though their views would be inconsistent with the bulk of current members). But most people will remain blissfully ignorant.

Thanks Will. This looks like a good time to advertise the online resources produced here at the SL Fed for educational purposes:

Deletehttp://www.stlouisfed.org/education_resources/econ-ed-online-learning/

The fact that the Fed remits its profit to Treasury isn't exactly exclusive to the fact that it is a cabal of bankers, when you consider that the Fed is primarily in the business of a) providing endless cheap money to crony banks around the world for the purposes of flipping sovereign debt, and b) absorbing any losses of this same class by diluting the public's currency.

DeleteOne would hope, ostensibly, that the Fed remits it's "profits" (perhaps loot would be a better word?) to the Treasury, since it is the public who presumably granted it the license to perpetually debase its currency. Unfortunately, the story doesn't quite end there.

Why don't we just do away with the middle man and let Treasury dilute our currency directly, without the smokescreen of monetizing public debt? After all, only an idiot would believe the argument for Fed "independence".

The only thing worse than the idea of politicians being able to engage in unlimited deficit spending (as of course they are now) would be to delegate the right to create money and credit ex nihilo to a quasi-private central bank.

Crackpot detected.

DeleteJust two views eh? Monetarist and Keynesian? How about the real bills view, which says that the fed's liabilities (including FR notes and reserves) are backed by the Fed's assets (including gold and bonds)?

ReplyDeleteMike,

DeleteNaturally, there are more than two views here, but I only had space to discuss the two dominant ones.

And, in any case, the "monetarist" view I described above sounds a lot like your "real bills" view, don't you think? Tell me how it is not.

The monetarist view says "Inflation, in the long-run at least, is determined by the supply and demand for currency". The real bills view says that inflation is determined by the assets and liabilities of the issuer of money, just like the value of any bond or share of stock is determined by the assets and liabilities of its issuer. You spoke about how the Fed needs assets to buy back its money, if money demand should fall. This rang a bell with me, since the real bills doctrine also says that the Fed needs assets, just like a firm that has issued stocks or bonds needs assets to impart value to those stocks and bonds.

DeleteSome scenarios where the two views differ:

1) US dollars become widely used in Mexico, and the Mexican central bank does not buy back an off-setting amount of pesos. Real bills says that this does not affect the Mexican central bank's assets or liabilities, so the peso would hold its value. Monetarism says the peso would lose value.

2) US dollars go overseas (to Mexico or wherever), and the Fed does not issue an off-setting amount of new dollars. Real bills says this does not affect the Fed's assets or liabilities, so no dollar deflation. Monetarism implies US deflation.

3) Some new kind of money (credit cards, gift cards, etc.) is introduced, and the Fed does not buy back an off-setting amount of FR notes. Real bills says no inflation, monetarism implies inflation.

Real bills also has a few things to say about what happens when the central bank's assets are denominated in its own currency, about shortages of currency, and a few hundred other things.

And you think I should have discussed this in my post?

DeleteWell, yes, freedom of speech notwithstanding, I think you should discuss a correct theory instead of two incorrect ones. Normally I don't chime in when people are discussing Monetarism/Keynesianism, but you were talking about the assets and liabilities of the central banks, which relates directly to the RBD. Then you said "Tell me how it is not.", which set off the preceding 300+ word rant.

DeleteAnd I thank you for the rant, but now tell me how any of the conclusions in my post would have changed if I had instead used the real bills doctrine?

DeleteAs far as I can tell, my "monetarist" view looks a lot like your RBD. I said that the value of assets held by the Fed back up the value of its liabilities. If the assets fall in value, there is a threat of dilution (inflation). Not sure how talking about the RBD would have contributed to the points I was trying to make.

Of the points you made about monetarism, I count 5 that would be viewed very differently from a real bills view. I'll focus on two:

Delete1) ". The flood of currency could potentially validate the higher inflation expectations -- a self-fulfilling prophesy"

If the public trades in some of its reserves for FR notes, the Fed's total liabilities are unchanged. Hence no change in the value of the dollar.

2) "The Fed's assets will decline in value. And with the decline in value, the ability to purchase cash"

Example: Suppose the fed has issued $60 of FR notes and $40 of reserves, backed by bonds worth $70 plus gold worth $30 (Call it 30 grams, so we have physical units.). Define E as the value of the dollar (grams/$). Since liabilities (100 units of money worth E grams each) must equal assets (30 grams + $70 of bonds, each dollar of which is worth E grams), we get

30+70E=100E

or E=1 gram/$.

But if the Chinese flood the market with US bonds, cutting their value in half, the above becomes:

30+35E=100E

or E=0.46 grams/$

This point (2) is not really different from yours, but it's more direct. Why tell the indirect story that loss of assets reduces the Fed's ability to suck up liabilities, which reduces the value of liabilities, instead of telling the direct story that loss of assets reduces the value of the Fed's liabilities? If we were taking about stocks and bonds, we'd just say that stocks and bonds issued by a firm will lose value if the firm loses assets, and skip the part about sucking up stocks and bonds.

Mike, my response to your points:

Delete[1] I don't think so. Suppose a company issues shares passively to meet nominal demand (unrealistic, but you know what I mean). Then a self-fulfilling dilution is possible. This is consistent with the RBD.

[2] OK, but now I think we are quibbling, no?

[1] If GM's assets are worth $60 billion, and the only thing on the liability side of GM's balance sheet is 1 billion shares, then each share will be worth $60. If GM issues 1 more share for $60 cash, then GM's assets rise in step with its issuance of shares, and GM's share price is not diluted. This will be the case whether the shareholders asked GM to issue the new share (i.e., the share was issued passively), or whether GM took the initiative in issuing the new share (i.e., the share was issued actively). If GM issued the new share and gave it away, then there is dilution, but no rational firm would ever do that. However, since the RBD says that liabilities are valued in accordance with the assets backing them, the above scenarios are all consistent with the RBD.

DeleteBut in any case, you were talking about issuing new paper money in exchange for reserves, which would be analogous to GM issuing new paper shares and swapping them for old shares that had existed only as bookkeeping entries, thus keeping total shares constant.

[2] The whole difference between the RBD and the quantity theory is that the RBD says money's value comes from asset backing, while the QT says that money's value comes from supply and demand. The story you tell creates a bridge between the two views by saying that assets allow the money issuer to create a money supply curve that is effectively horizontal at a level determined by asset backing. Most quantity theorists don't take that approach, and they talk as if the Fed's assets are irrelevant and the dollar is fiat money. If you are in that small group that thinks that the Fed's assets matter, then welcome to the club, but that stuff about "sucking up liabilities" seems like a barbarous relic from the pure quantity theory.

1. Super informative

ReplyDelete2. Conspicuously absent from the theory of inflation above is any role played by the money supply.

Can you discuss further?

There are plenty of non-monetary theories of inflation. One way to think of it is as follows. Consider the famous equation of exchange PY = MV. Hold real GDP (Y) and velocity (V) fixed. Then the simple Quantity Theory of Money tells us that the price-level (P) is proportional to the money supply (M). A monetarist assumes that the Fed controls M, and therefore controls P. But the NK assumes that P is determined by price-setting behavior, and that the money supply simply accommodates itself to the prevailing price-level. The direction of causality is reversed in this latter case.

DeleteDavid, it seems to me that my friend, Mr. Franklin, disproved the NK model almost 300 years ago when he started printing paper currency for Pennsylvania.

DeleteYou will recall that the import business required the export of gold and silver, for one had to pay in advance, leaving a shortage of money. This shortage was a perpetual and well understood problem.

The Fed has several publications very descriptive of the problem and Franklin's solution.

Do facts no longer matter?

Facts do matter. And one fact is the development of financial markets and record-keeping since your time. It may be the case that the monetarist view constitutes a good approximation for more primitive economies, the NK view for more advanced economies. Reality likely lies in between these two extremes.

DeleteDavid

DeleteWhat a fun reply!

BTW, could you list several monetarists. I would certainly like to quote you as writing, their "view constitutes a good approximation for more primitive economies."

Please please let one be Friedman and a second be Taylor or Lucas.

Last, where does this put Lord Keynes, in the reality that likely lies in between the two extremes, I hope?

Beyond that, whom else can we can consign to the dustbin for only offering a good approximation for more primitive economies. Any chance that will take out the invisible hand of Smith and open up a few minds to the "reflexive process" of Soros in which what happens in an economy is participants' biased decisions interacting with a reality that is beyond their comprehension?

Just to be clear, I use "more primitive" to mean less than perfect financial markets. Woodford likes to consider the extreme case of a "cashless" economy. Some economies are closer to that state than others. But in any case, one should be careful in assigning labels like "monetarist" or "Keynesian" to any one particular view.

DeleteIs cashless extreme or is it the end the game?

DeleteAnd, instead, Why are both models of no use because they have no fourth factor of production: information?

There are four factors of production, of which the most important is information for information is a substitute for all the others. Information will shortly be able to turn lead into gold. When machines can build, design, repair, and replace themselves, will there be any role for labor or capital (including money)?

And, on a separate track, we are approaching a point where our ability to write and enforce contracts making forward promises will replace any need for capital (or money). Units or measures of exchange may well, themselves, become ever less important. Consider a totally robotic store where the only cost is of the raw materials in the products and packaging and replacement parts.

Given that we can see this just over the horizon, who is to say that today is not an accurate reflection of future expectations, a world in which neither labor nor capital have value? Doesn't that picture most accurately mirror reality?

In particular, if information is a substitute for capital, what does that do to the so-called real rate of interest? Are we seeing low rates of interest and lack of aggregate demand because our future expectations are that capital will have no value?

In sum, if you want to picture the past as primitive, doesn't the known future tell us such is equally true for the current models you have outlined above?

The amount of misunderstanding of basic economics that John D managed to pack into these posts is staggering.

DeleteThe assets on the Fed balance sheet represent losses that otherwise would have accrued to the Fed's cronies, but instead those cronies were subsidized by the currency holder/taxpayer.

ReplyDeleteThe $89 billion remitted to the US Treasury represents nothing more than the proceeds of the seigniorage tax, minus of course the Fed's own operating expenses which include paying dear Mr. Andolfatto's salary. Apparently we should be impressed that an entity delegate the legal right to counterfeit money showed a nominal profit.

There isn't much "inflation" because the way that inflation is measured does not include financial asset prices, specifically bond prices. The new money is being used to bid up the prices of financial assets, resulting in arbitrary and perhaps not-so-arbitrary winners and losers in a giant game of musical chairs. Meanwhile, we have a bond market bubble, and anyone fortunate enough to frontrun the Federal reserve for the last decade or so in that market has made enormous, illicit gains.

The scam is wearing thin.

Tippit, the last time I checked, one cannot actually eat a financial asset. The CPI (consumer price index)I report above is a measure of the cost of a "typical" basket of consumer goods and services -- you know, the things that actually have a direct bearing on material living standards.

DeleteI think the division between "New Keynesian" and "New Monetarist" to a certain extent obscures the fact that they are largely equivalent theories looked at through different lenses. Although New Keynesian models take a short-cut by simply assuming that the Fed sets the nominal interest rate by fiat, the implicit assumption is that it does this through balance sheet operations. In that regard, New Monetarist theories are basically just New Keynesian theories but with an explicit framework about how the Fed achieves interest rate targets.

ReplyDeleteHow is the fact that you cannot eat a financial asset relevant to the fact that wealth is being transferred via this process? I can sell financial assets, even government bonds, and use the capital gains to buy food. Or I can buy rental real estate, and let the peasants pay for my food as they pay their rent.

ReplyDeleteThe fact that as others lose their jobs as the real economy implodes due to the Fed-induced malinvestment does tend to hold down CPI-measured "inflation" though.

Are you, David Andolfatto, proclaiming from your ivory tower that the Fed's manipulation of asset prices doesn't matter?

Tippit:

DeleteEarlier you said:

There isn't much "inflation" because the way that inflation is measured does not include financial asset prices, specifically bond prices.

And now you say:

The fact that as others lose their jobs as the real economy implodes due to the Fed-induced malinvestment does tend to hold down CPI-measured "inflation" though.

So, if I understand you correctly, you are blaming the Fed for increasing the returns on pension funds and other savings, while at the same time keeping the cost of living in check.

There's no pleasing some people, it seems.

Actually, I'm blaming the Fed for a massive, surreptitious, and regressive transfer of wealth. Not all bondholders are pensioners, as if this were relevant. Are you really saying that the Fed's financial repression is "increasing the returns on savings"? Can you even say that with a straight face? It's increasing the capital gains for bondholders, stockholders, and select Fed cronies, at the expense of everyone else (no, not everyone owns financial assets, Mr. Andolfatto).

DeleteSo, once again, do you maintain that the Federal Reserve's manipulation of financial asset prices doesn't matter?

Miss Tippit:

DeleteYOU are the one saying that the Fed has increased the return to saving (the Fed is inflating asset prices, remember?).

Sure, not everyone owns assets, but for those that do not, even you admitted that the Fed is keeping the cost of living (CPI inflation) low.

So, implicit in your assertion is that saving = investing in assets. Funny, I thought saving meant saving money, either in a bank account paying anemic interest rates, or under a matress - the exact opposite of your definition of saving. In fact, the cost of living should be a lot lower, so that the unemployed as a result of Fed policy could afford to live. In fact, the benefactors of Fed policy, first and foremost its money center bank cronies, and secondly those who are fortunate enough to own assets so that they are at least somewhat insulated from the Fed's perpetual debasement are the only ones bidding for consumer goods. Everyone else is busy looking for a job.

ReplyDeleteYou seem to have a hard time answering a very simple and direct question Mr. Andolfatto. Does the Fed's manipulation of financial asset prices matter?

No, I don't think it matters: you will remain a troll whether or not the Fed changes its policy rate.

DeleteI can assure you that I'm not a troll, and that everything I typed was in earnest. I don't want the Fed to change it's policy, I want the Fed to be abolished, all of its cronies and benefactors in jail, and you out of a job.

Deletebenefactors in jail

DeleteEt Tu? (for like it or not, you have been a benefactor).

Tippit, you missed the first day of economics. There is no rule or law of economics saying that the amount of money available to be lent is equal to the amount of good loans. No rule of economics says that stocks or bonds are fairly valued.

Life in an advanced society is a confidence game, played on the same golf course where Bobby Jones triumphed, the six inches between your ears. Money, finance, etc., are all man-made, suffering from the same human flaws as all other endeavers. Do your parents, spouse, children, and friends view you are more or less flawed than the Fed?

Get online. Spend a very few dollars on Soros, The Open Society, then chill.

Presently you merely sound jealous. You, like everyone else, what the best of both worlds. You want the value of your house to go up, but your assessed value and taxes to go down. The World doesn't work that way.

Congrats, John D, you seem to have located a bigger crackpot than yourself. I honestly didn't think that was possible. I will now pursue both of you until you stop polluting things with your nonsense. You're on notice, Tippit, I will mock you mercilessly until you depart this honorable blog.

DeleteTippit,

DeleteDon't let the Anon. troll get you down. He is an econ prof so bad at his trade he won't use his name or write his on blog.

Just disregard him. David is a straight up guy and you ought to read him with great care.

And,if it makes you feel better, we are all jealous of Jamie Dimon and JPMorgan. But, with the House in control of Republicans and with the Senate subject to filibuster, nothing is ever going to be done about it. It is called "divided government." I suspect the people at the Fed are as jealous as you when it comes to Dimon and JPMorgan.

Alexander, I am not a benefactor of the Fed. I have a portfolio which includes precious metals with bases in about $270/oz for gold and $5/oz for silver, as well as real estate, and stocks. The unrealized gains in precious metals will be taxed at a 28% "collectible" rate, which is of course designed to punish gold owners. The "tax on the inflation tax" which accrues to the metals is ridiculous, and I'm not benefitting from the Fed's action as much as I'm merely not falling behind, like most people. The real benefactors of the Fed are the banks who, for example, get to perpetually borrow from it at 25 basis points, and then flip that into Greek debt yielding 1500 basis points, knowing full well in advance what the bailout policy of the IMF will be.

DeleteI am not an economist, I am a philosopher, and I like to view things as simply as possible (but no simpler, as Einstein would put it). The Fed is a glorified counterfeiting operation. Nothing more, nothing less. All of the economists, apologists, and academics can't change that fact. I don't pretend that stocks and bonds should be fairly valued all the time, but this is not an argument for the perpetual manipulation of financial asset prices. Why would I spend a dime on George Soros? He's a criminal and a clown.

I'm not jealous, I'm angry. Angry at what the monetary and banking system are doing to the world, and angry at the inability of most people to see it for what it is. If I were jealous, I would have moved to Wall Street or Washington and joined the legions of hardcore criminals and fraudsters a long time ago. I cannot be jealous of morally and intellectually bankrupt people. As for Andolfatto, he is merely a Fed apologist, and, as such, is the enemy. He failed to answer even a simple question about asset prices, and, in the usual fashion of most academics and apologists, obfuscated the issue. If I wanted to hear obfuscatory lies, why would I read Andolfatto when I can simply read or listen to Bernanke instead? The reason I am here is because I would like to see him attempt to defend what is, ultimately, indefensible.

Anonymous:

You haven't said anything substantial, so your mockery is pointless. This blog is more or less a joke. I'm here, once again, to see Andolfatto attempt to defend the indefensible, and I will depart when it becomes tiresome or boring to do so, just as I have before.

Andolfatto:

Don't take my attitude too personally. This is how normal people react when they're fed lies and spurious rationalizations, as you do repeatedly. Make no mistake about it, I hate the Fed, and it's defenders. I defy you to answer any of my questions sincerely, as they were asked, even though they are rhetorical.

Tippit, seems to be no helping you

DeleteThe dollar is rising in value. So much for your currency debasing theory.

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/03/14/the-dollar-is-soaring-heres-what-that-should-tell-us-about-the-economy/

The article also tends to explain that the actions of others effects us. Closing up the Fed will only leave us subject to further manipulation by others. Oh well, so much for reality.

For those who understand economics, which does not include our other anon. troll, here is a link to a couple of very interesting charts, the first showing the decline of interest rates since 1990, from 9 to near zero

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/03/13/washington-hates-deficits-why-it-hates-them-is-less-clear/?wprss=rss_ezra-klein

If information, the fourth factor of production, is a substitute for capital, that would be expected behavior.

If you are so old school that you cannot understand information being a separate and distinct factor of production, well I cannot help you. All I can say is go back to Coase and start again, paying especially attention to Drucker.

It should, however, be apparent to anyone who considers such, that we are going to need an entirely new economics, an economics of information, well before all production is done by machines that build, repair, and replace themselves. We are also going to need a new Social Contract and form of Government.

But, with our legion of economists trained only in the worship of dead economists who ever considers, writes, or talks about the how distinctly different the future of economics is going to be from the past, or about how expectations of that future are affecting actions today.

No, we have dullards who think that their simple model that in 2030 we will have so many people on SS means something and we can project a deficit. We are getting ready for the Lightning Round but have few players standing and none, probably save Brad Delong, capable of scoring.

http://wraltechwire.com/our-future-will-be-brighter-than-you-think-but-more-disruptive/12185002/

DeleteAn interesting link on the near term arrival of unlimited energy and water, two additional game changers for economic models.

Tippit and John D, two crackpots in a pod. Sad, angry little men who think the world owes them something, but aren't quite smart enough to figure out why they've failed in their lives.

DeleteSo currency debasement and the dollar rising at times is not mutually exclusive. The value of dollars is dependent upon the supply of dollars, the demand for dollars, and the supply and demand of and for the things that dollars can buy, whether it's goods and services, or foreign exchange.

DeleteThis graph of M2 indicates quite clearly that we have had nonstop currency debasement since 1995:

http://research.stlouisfed.org/fred2/series/M2

So why isn't this reflected in consumer prices?

1) The consumer price index is doctored so as to manage entitlement costs. How much so is up for debate.

2) Productivity gains continue to offset currency debasement. Unfortunately consumers rarely see lower prices, and this wealth is transferred to non-producing actors who are friends of the Federal Reserve System.

3) Asset prices have absorbed most of this new money, which is why bond yields are just off all-time lows, and global bond markets (with a few exceptions) are in bubble territory.

4) Malinvestment caused by the Fed's perpetual subsidy of bondholders has served to destroy productive capital and shifted it to the government sector, causing massive private sector layoffs, and a decline in consumer demand. Prices have not cratered, because non-producers who enjoy Fed-sponsored capital gains continue to consume.

All of this represents a regressive and inequitable transfer of wealth, regardless of what happens to the general price level. This is an important concept to grasp. Even if the so-called "cost-of-living" appears low, there is massive wealth condensation as financial asset prices diverge from historical norms. These are but a few reasons why the Fed must be abolished.

So sad. What if you wrote an entire rant and no one answered?

DeleteTippit,

DeleteYou might want to see how you score on this test:

http://math.ucr.edu/home/baez/crackpot.html

I'm guessing your number will be quite high. John D, you are invited as well.

Wow, Tippit really is a nutjob. Just look at the link on his name, it's like something out of a birther/truther wet dream.

ReplyDeleteTippit calls himself a philosopher, which amounts to admitting he is a useless and/or parasitic member of society.

ReplyDelete