About a year ago, Jim Bullard criticized the argument that that the Fed was missing on both sides of its dual mandate. Mark Sadowski (who should have his own blog, I think) has asked me to post his reply. I am most happy to do so.

=======================================

=======================================

This

is written in response to a question David Andolfatto posed in September in a

blog post entitled “Is the Fed missing on both sides of its dual mandate?”

David

concluded that post with the following statement:

“Bullard suggests that a non-monotonic

transition path for inflation is unlikely to be part of any optimal path in a

NK [New Keynesian] type model. The optimal path for inflation is unlikely to be

part of any optimal path in a NK type model. The optimal transition dynamics are

typically monotonic—think of the optimal transition path as a movement back up

the PC [Phillips Curve] in the diagram above. If this is true, then the optimal

transition path necessarily has the Fed missing on both sides of its dual

mandate.

Of course, conventional NK models frequently abstract from a

lot of considerations that many people feel are important for understanding the

recent recession and sluggish recovery. The optimal monetary policy may indeed

dictate "inflation overshooting" in a different class of models.

Please feel free to put forth your favorite candidate. Tell me why you think Bullard

is wrong.”

James

Bullard, President of the St. Louis Fed, had just written an opinion piece for

the Financial Times where he stated:

“To

argue against monotonic convergence now would imply that when unemployment is

above the natural rate, monetary policy should aim for inflation above the

Fed’s 2 per cent target. On the face of it, this does not make sense: the US

has experienced periods when both inflation and unemployment have been above

desirable levels. In the 1970s this phenomenon was labeled stagflation.

Monetary policy has been regarded as poor during that period.”

At

the time Scott Sumner mockingly responded:

“To

argue for monotonic convergence now would imply that when unemployment is above

the natural rate, monetary policy should aim for inflation below the Fed’s 2

per cent target. On the face of it, this does not make sense: the US has

experienced periods when both inflation and employment have been below

desirable levels. In the 1930s this phenomenon was labeled “The Great

Depression.” Monetary policy has been regarded as poor during that period.”

Sumner

is of course talking about the contractionary portion of the U.S. Great

Depression. The subsequent 1933-37 recovery, during which real GDP grew at an

average rate of 9.5%, is an excellent example of “oscillatory convergence” with

unemployment high and falling and inflation higher than normal. And yes, monetary

policy is generally regarded as excellent during that period.

Andolfatto’s,

Bullard’s, and Sumner’s comments raise a great many questions. For example, what

is the relationship between unemployment and inflation? How has this

relationship changed over time, and why? How has this relationship been modeled

over time? How should this relationship affect the conduct of monetary policy? For

the moment, at least, I want to stay focused on Bullard’s remarks.

As

evidence Bullard cited a paper by Frank Smets and Raf Wouters, “Shocks and

Frictions in US Business Cycles – A Bayesian DSGE Approach” (American Economic

Review, Vol. 97, No. 3, June 2007, pp. 566-606). In an essay published about a

month later, “Monetary Policy and the Expected Adjustment Path of Key

Variables” (Federal Reserve Bank of St. Louis Economic Synopses, 2012, No. 30),

Bullard clarified his Financial Times comments:

“Let’s

consider the medium-sized macroeconomic framework of Smets and Wouters (2007).

This is an important benchmark model; and, while we could argue about the

details, I think it will serve to make my point. In the Smets and Wouters

dynamic stochastic general equilibrium (DSGE) model there are many shocks, and

there is a monetary policymaker that follows a Taylor-type monetary policy rule

not unlike ones used in actual policy discussions. The authors estimate their

model using postwar U.S. data, and they also report results for subsamples

including the post-1984 data. Importantly, what the authors are estimating is a

general equilibrium for the economy, which includes monetary policy.

How

does the economy adjust in the Smets and Wouters model? The chart is Figure 2

from their paper.

The

authors plot the reaction of key macroeconomic variables to three types of

shocks in their model that might be thought of as demand shocks. Variables are

reported as deviations from a steady-state value, so that zero represents a

return to normal. The variables include inflation and a labor market

variable—hours worked. Time is measured in quarters. The shock is a positive

one—output and hours go up in response—but the story is merely transposed for a

negative shock (i.e., flip the figures upside down).

The

reaction of all variables is essentially monotonic beyond the hump in these

graphs, at least through year four. (That is, the adjustment does not show much

of a tendency to oscillate about the long-run value.) For all three types of

demand shocks, the Fed would be “missing on both sides of the dual mandate”

almost all of the time as the economy recovers from the shock. If the shock

were negative, hours would be too low (unemployment too high), and inflation

would be too low every quarter for many years. Yet the monetary policy embedded

in this general equilibrium is a Taylor-type policy rule that has often been

argued to closely approximate the optimal monetary policy in frameworks such as

this one. 2 It is in this sense that I do not think merely observing where

inflation and unemployment are relative to targets or long-run levels at a

point in time is telling us very much about whether the monetary policy in use

is the appropriate one or not.”

Footnote

2 reads:

“One

can investigate optimal-control monetary policy assuming credible commitment in

this model, taking the non-policy parameters as estimated by Smets and Wouters.

This type of monetary policy changes these impulse response functions but still

leaves goal variables “missing on both sides of the mandate” in many

situations. I thank Robert Tetlow for investigating this issue in response to

an earlier draft.”

The

monetary policy reaction function that is built into the Smets and Wouters

(2007) model is the original rule John Taylor proposed in 1993 ("Discretion

versus Policy Rules in Practice", Carnegie-Rochester Conference Series on Public

Policy, Vol. 39, December 1993, pp. 195-214), namely a Taylor Rule that places

equal weights on the inflation gap and the output gap. In 1999 Taylor discussed

an alternative version of this rule that placed double the weight on the output

gap than on the inflation gap, (“A Historical Analysis of Monetary Policy

Rules”, Monetary Policy Rules, Chicago: University of Chicago Press, pp.

319-341). This is a point to which we shall return later. Thus the response of

the economy to the demand shocks illustrated in Figure 2 is conditional on the

Taylor Rule embedded in the model.

At

this point it might be worth mentioning that one of the acknowledged

shortcomings of medium-scale New Keynesian DSGE models is that typically there

is no reference to unemployment. Bullard infers the impact of a demand shock on

unemployment from its effect on hours worked. In particular, the Phillips Curve

in the Smets-Wouters model is a hybrid New Keynesian type in which inflation

depends on past inflation, expected future inflation, current price mark-up and

a price mark-up disturbance. Apparently the only reference in the model to the

output gap occurs in the model’s monetary policy reaction function (i.e. the

Taylor Rule).

Bullard’s

footnote on optimal control monetary policy is especially relevant in this

context. What is “optimal control” monetary policy? Federal Reserve Vice Chair

Janet Yellen spoke about optimal control techniques in speeches in April, June

and November of last year. Here is how she introduced them in April:

“One

approach I find helpful in judging an appropriate path for policy is based on

optimal control techniques. Optimal control can be used, under certain

assumptions, to obtain a prescription for the path of monetary policy

conditional on a baseline forecast of economic conditions. Optimal control

typically involves the selection of a particular model to represent the

dynamics of the economy as well as the specification of a "loss

function" that represents the social costs of deviations of inflation from

the Committee's longer-run goal and of deviations of unemployment from its

longer-run normal rate. In effect, this approach assumes that the policymaker

has perfect foresight about the evolution of the economy and that the private

sector can fully anticipate the future path of monetary policy; that is, the central

bank's plans are completely transparent and credible to the public."

In

that speech Yellen describes how projections generated by FRB/US, the Federal

Reserve’s primary forecasting model, were adjusted to replicate the baseline outlook

constructed using the distribution of FOMC participants' projections for

unemployment, inflation, and the federal funds rate that were published in

January of that year. A search procedure was used to solve for the path of the

federal funds rate that minimized the value of a loss function. The loss

function was equal to the cumulative sum from 2012:Q2 through 2025:Q4 of three

factors: 1) the discounted squared deviation of the unemployment rate from

5-1/2 percent, 2) the squared deviation of overall PCE inflation from 2

percent, and 3) the squared quarterly change in the federal funds rate. She

termed this path the “optimal control” path.

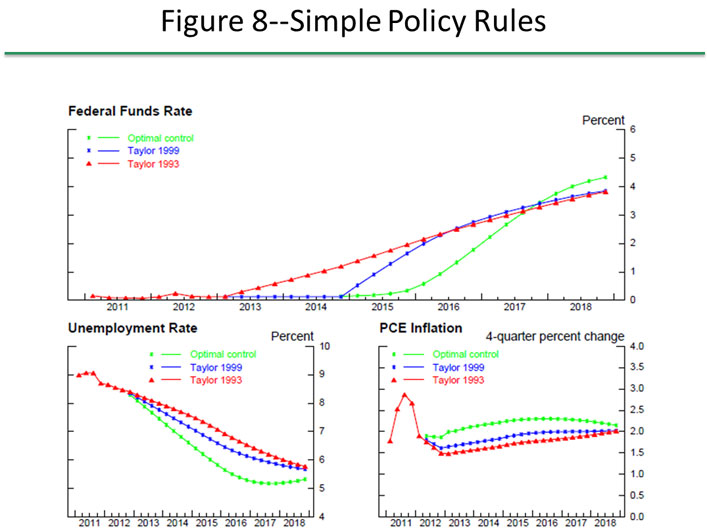

Yellen

also used the FRB/US model to construct the federal funds rate path called for

by the 1993 and 1999 versions of the Taylor Rule conditioned on the same

illustrative baseline outlook used to generate the optimal control path. These paths,

as well as the optimal control, and the various resulting paths for

unemployment and inflation are depicted in Figure 8 of her speech:

{kind=link}

The

1993 Taylor Rule calls for the federal funds rate to begin rising in 2013Q2.

The 1999 Taylor Rule calls for the federal funds rate to begin rising in

2015Q1. Optimal control calls for the federal funds rate to begin rising in

2015Q4. More importantly, note that whereas the paths for unemployment and

inflation under the Taylor Rules converge monotonically, under optimal control they

display oscillatory convergence, with both unemployment and inflation

“overshooting” before converging to their long run values.

Now,

it’s true these results were generated with FRB/US and not the Smets-Wouters model.

FRB/US is a somewhat older (1997), large-scale simultaneous equation

macroeconometric model. But because expectations of future economic conditions

are explicit in many of its equations, and adjustment of nonfinancial variables

is delayed by frictions, it too is often described as New Keynesian. The

dynamic adjustment of its aggregate price equation means that, like the Smets-Wouters

model, inflation is dependent on past inflation, expected future inflation and

the current price markup, as well as number of additional variables such as the

unemployment rate, energy prices, etc. And the general effect of monetary

policy shocks on output, inflation and interest rates is quite similar to the

Smets-Wouters model.

Thus

I expect were one to investigate optimal control monetary policy assuming

credible commitment using the Smets-Wouters model, as Bullard mentions the

possibility of in his footnote, one would probably find results similar to

those generated with the FRB/US model assuming it were subject to the same loss

function. To be more explicit, under the same assumptions, an optimal control

path generated by the Smets-Wouters model would very likely exhibit the same

oscillatory convergence pattern of unemployment and inflation as demonstrated with

the FRB/US model.

Thus

it seems to me that the primary issue here is not what type of model should be

used, but what the goals of monetary policy should be. Should monetary policy

be guided by simple rules, such as the Taylor Rules, because in the past, and under

potentially very different conditions, they were considered optimal? Or should

monetary policy be more explicitly guided by the mandates to which it is legally

subject? Or, indeed, should monetary policy be guided by something else

entirely?

Mark Sadowski

Mark Sadowski

Excellent post. I'd add a minor comments to what Mark already covers here:

ReplyDelete- he is exactly right in pointing out that there is no reason to suspect the Taylor rule is anywhere near optimal, and so we should avoid relying too much on it - and its implication for the impulse response of key variables - to inform policy;

- while the loss function minimisation procedure is an important improvement, we should also look at analysing Taylor-type rules in environments where the intertemporal welfare function is what we want to optimise. Obvious corollary is that a rule may minimise the loss function and still impose a welfare loss relative to a rule chosen to optimise the intertemporal welfare function;

- a technical point relates to how the output gap is defined: whether we optimise a loss function or the intertemporal loss function, defining the output gap as the difference between realised output and the steady-state level may lead to a different rule relative to a scenario in which the gap is defined as the difference between output and the output level in the absence of any frictions (essentially the output level in a simple RBC model);

- a final consideration pertains to the robustness of rules. Because we don't know which models are closer to the truth (price vs wage rigidity, Rotemberg or Calvo pricing, KM or BGK type financial constraints, etc..), we want rules that are robust to different types of specifications, which will almost definitely come at the cost of sub-optimality in each individual model.

All in all, excellent post!

There is, of course, no reason at all why the squared quarterly change in the federal funds rate should be part of the loss function. Indeed, I suspect that one reason the markets tanked after Chairman Bernanke's post-FOMC press conference was his emphasis on smoothing policy. He repeatedly stressed that any policy changes would be gradual and unsurprising. The implication is that it's perfectly OK if a few hundred thousand or million people have to go without work for a few months to make life more comfortable for bankers and central bankers.

ReplyDeleteGood point!

DeleteI completely agree that Mark Sadowski should have his own blog!

ReplyDelete