Some time ago I wrote about the prospect of the U.S. economy going through a Canadian-style slump (see here). To summarize: The recession that hit Canada and the U.S. in the early 1990s was much more severe in Canada than in the U.S., and the recovery in Canada took almost a decade to complete. In 2008, the tables appear turned. In what follows, I plot the employment-to-population ratio for Canada from 1989:1 - 2003:1 and match it up against the same ratio for the U.S. beginning in 2007:1 - present. The parallels thus far are striking.

Let's start with the employment ratios (courtesy of my able research assistant, Li Li) for the whole population in both countries: (All starting points normalized to 100 -- the actual employment rates are close in any case.)

This shows that the slump, as measured by the drop in employment, was about the same magnitude for Canada in 1990-91 as for the United States in 2008-09. The recovery dynamic in both cases appears to be painfully slow.

This shows that the slump, as measured by the drop in employment, was about the same magnitude for Canada in 1990-91 as for the United States in 2008-09. The recovery dynamic in both cases appears to be painfully slow.

Let's now decompose employment across various age groups.

In terms of young and prime-age workers, the U.S. looks a little more depressed relative to the Canadian experience. The experience of older U.S. workers seems less depressed (but the behavior of older workers since the mid 1990s is influenced by a change in secular dynamics, so perhaps should not be viewed as a recovery dynamic.)

Now let's decompose by age and sex. Here we have the data for adult men:

And here we have the age-sex decomposition for men:

The correspondence between those aged 20-55 (the bulk of the population) is very close. Here is the data for adult females:

And here is the age-sex decomposition for women:

The most recent U.S. recession is sometimes labeled a "mancession" in reference to the fact that men appear to have been particularly hard hit (my colleague Silvio Contessi and my RA Li Li talk a bit about this phenomenon here.) It is interesting to note that while this may have been the case, the data here suggest that U.S. females were nevertheless hit harder than their Canadian counterparts in the 1990s.

Just for fun, I asked Li Li to plot broad stock market indices: the TSX composite index for Canada and the S&P 500 for the U.S. (both series have been adjusted for inflation).

Anyone willing to bet against the EMH?

At this point, I'm not entirely sure how to interpret this data. My feeling is that something useful may come out of studying the Canadian episode in greater detail. Maybe a few Ph.D. students are willing to take up the challenge?

Let's start with the employment ratios (courtesy of my able research assistant, Li Li) for the whole population in both countries: (All starting points normalized to 100 -- the actual employment rates are close in any case.)

Let's now decompose employment across various age groups.

In terms of young and prime-age workers, the U.S. looks a little more depressed relative to the Canadian experience. The experience of older U.S. workers seems less depressed (but the behavior of older workers since the mid 1990s is influenced by a change in secular dynamics, so perhaps should not be viewed as a recovery dynamic.)

Now let's decompose by age and sex. Here we have the data for adult men:

And here we have the age-sex decomposition for men:

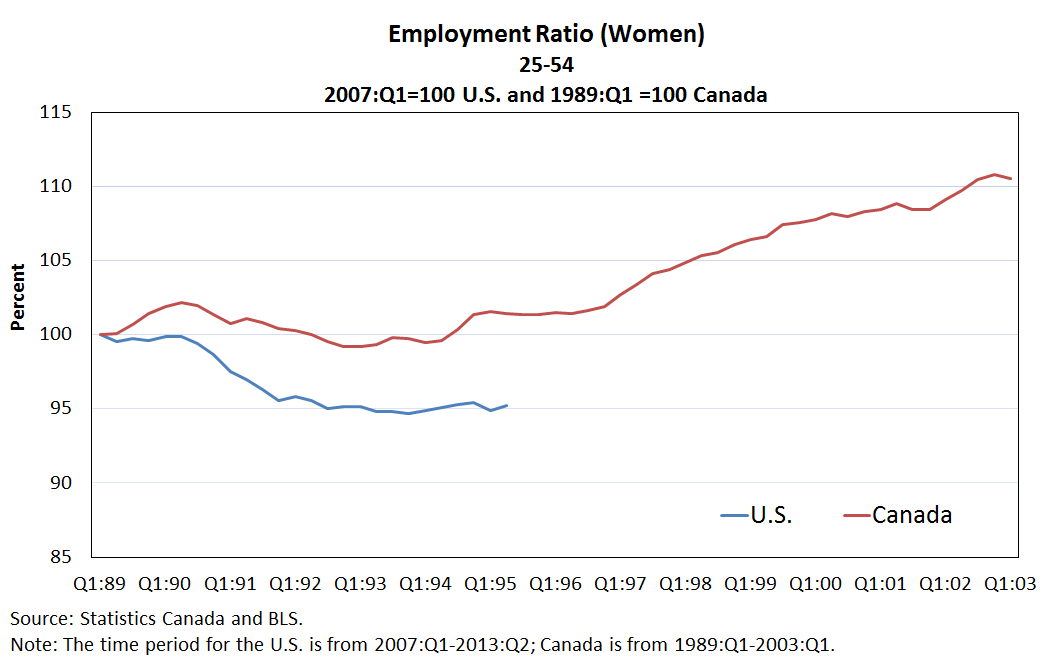

The correspondence between those aged 20-55 (the bulk of the population) is very close. Here is the data for adult females:

And here is the age-sex decomposition for women:

The most recent U.S. recession is sometimes labeled a "mancession" in reference to the fact that men appear to have been particularly hard hit (my colleague Silvio Contessi and my RA Li Li talk a bit about this phenomenon here.) It is interesting to note that while this may have been the case, the data here suggest that U.S. females were nevertheless hit harder than their Canadian counterparts in the 1990s.

Just for fun, I asked Li Li to plot broad stock market indices: the TSX composite index for Canada and the S&P 500 for the U.S. (both series have been adjusted for inflation).

Anyone willing to bet against the EMH?

At this point, I'm not entirely sure how to interpret this data. My feeling is that something useful may come out of studying the Canadian episode in greater detail. Maybe a few Ph.D. students are willing to take up the challenge?