I recently gave a short presentation to the Board of Directors of the Louisville branch of the St. Louis Fed. Following my presentation (which stimulated a lively discussion), I had the opportunity to listen to each member report on local economic conditions from different parts of Kentucky. Two themes stood out. The first was how "an air of uncertainty" along a variety of dimensions had "frozen" investment plans (with the apparent exception of younger entrepreneurs, who probably do not know any better-jk). The second was the unfilled demand for highly skilled, specialized workers (primarily in manufacturing).

I want to focus on the second theme here. In some sense, it is really amazing that firms are struggling to find qualified workers in an era of 8% unemployment. The Financial Times recently ran a piece on the subject: Skills Gap Hobbles US Employers, and I have to say that Mr. Greenblatt below would have fit right in at my BOD meeting:

Apart from anecdotal evidence, how does one go about measuring "skills mismatch caused by structural shock?" One idea, initially proposed by Abraham and Katz (JPE, 1986), is to use the comovement to in vacancy and unemployment rates to identify "cyclical" and "structural" shocks.

I put those terms in quotes because there are no set definitions for them. I like to think of a cyclical shock as an event that makes it more or less profitable to find the same kind of worker for the same kind of job. And I like to think of a structural shock as an event that makes it more or less profitable to find a different kind of worker for a different kind of job.

Anyway, the Abraham and Katz idea is that one would expect cyclical shocks to trace out a stable, negatively-sloped Beveridge curve. That is, one would expect the job-vacancy rate and the unemployment rate to move in opposite directions. A structural shock, by contrast, is expected to move vacancy and unemployment rates in the same direction. The idea here is that it is now more difficult to find the right kind of worker, so that even greater levels of recruiting intensity is likely to be associated with higher unemployment rates.

Anyway, the Abraham and Katz idea is that one would expect cyclical shocks to trace out a stable, negatively-sloped Beveridge curve. That is, one would expect the job-vacancy rate and the unemployment rate to move in opposite directions. A structural shock, by contrast, is expected to move vacancy and unemployment rates in the same direction. The idea here is that it is now more difficult to find the right kind of worker, so that even greater levels of recruiting intensity is likely to be associated with higher unemployment rates.

The FT article cited above uses this idea in the diagram to the right (together with the results of a Kaufman poll of entrepreneurs) to suggest that the high U.S. unemployment rate is primarily the consequence of "structural" factors.

Here is what the U.S. Beveridge curve looks like from May 2005 - November 2011 (The vacancy rate is computed from the Conference Board's help-wanted-online data, which is available from 2005 only).

I want to focus on the second theme here. In some sense, it is really amazing that firms are struggling to find qualified workers in an era of 8% unemployment. The Financial Times recently ran a piece on the subject: Skills Gap Hobbles US Employers, and I have to say that Mr. Greenblatt below would have fit right in at my BOD meeting:

Drew Greenblatt has been looking for more than a year for three sheet-metal set-up operators to work day, night or weekend shifts.

The president of Marlin Steel Wire Products, a company in Baltimore with 30 employees, Mr. Greenblatt says his inability to find qualified workers is hampering his business' growth. "If I could fill those positions, I could raise our annual revenues from $5m to $7m," he says.

He is offering a salary of more than $80,000 with overtime, including health and pension benefits. Yet in spite of extensive advertising, he has had no qualified applicants. He is trying to train some of his unskilled staff but says none has the ability or the drive to complete the training.This quote identifies two problems. The first is what economists call "skills mismatch" caused by a "structural" shock. The second, that some workers are unwilling and/or unable to upgrade their skills is another matter that deserves attention, but is something that I will leave aside here.

Apart from anecdotal evidence, how does one go about measuring "skills mismatch caused by structural shock?" One idea, initially proposed by Abraham and Katz (JPE, 1986), is to use the comovement to in vacancy and unemployment rates to identify "cyclical" and "structural" shocks.

I put those terms in quotes because there are no set definitions for them. I like to think of a cyclical shock as an event that makes it more or less profitable to find the same kind of worker for the same kind of job. And I like to think of a structural shock as an event that makes it more or less profitable to find a different kind of worker for a different kind of job.

Anyway, the Abraham and Katz idea is that one would expect cyclical shocks to trace out a stable, negatively-sloped Beveridge curve. That is, one would expect the job-vacancy rate and the unemployment rate to move in opposite directions. A structural shock, by contrast, is expected to move vacancy and unemployment rates in the same direction. The idea here is that it is now more difficult to find the right kind of worker, so that even greater levels of recruiting intensity is likely to be associated with higher unemployment rates. The FT article cited above uses this idea in the diagram to the right (together with the results of a Kaufman poll of entrepreneurs) to suggest that the high U.S. unemployment rate is primarily the consequence of "structural" factors.

Here is what the U.S. Beveridge curve looks like from May 2005 - November 2011 (The vacancy rate is computed from the Conference Board's help-wanted-online data, which is available from 2005 only).

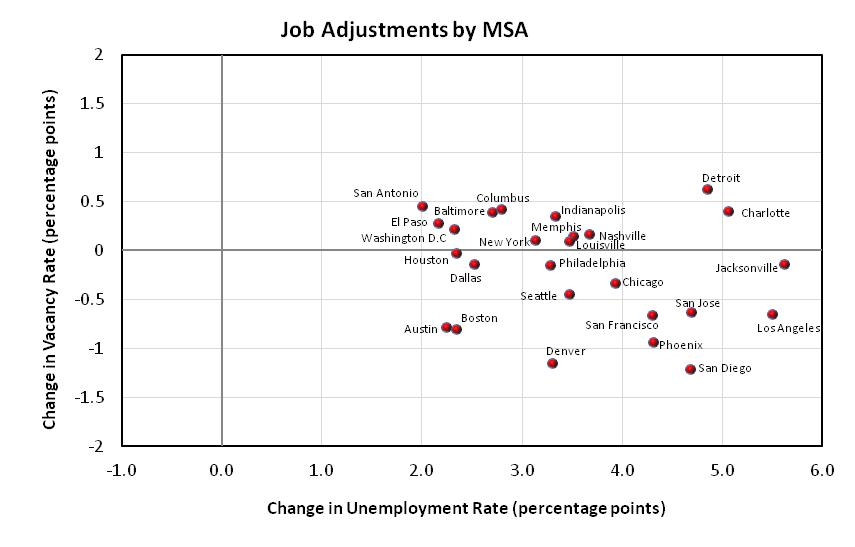

As the HWOL measure of job vacancies is available at the city level, Constanza Liborio and I thought it might be interesting to see how

job availability varies across major U.S. metropolitan areas and how job

vacancy rates correlate with regional unemployment rates before and after the beginning

of the most recent recession.

Specifically, the exercise we perform is as follows. Consider a major U.S. metropolitan area. Compute the

average job vacancy rate and unemployment rate for this metropolitan area over

the prerecession period May 2005 – November 2007. Recalculate these averages

since the beginning of the last recession, December 2007 – November 2011. Next, compute the change in the

vacancy rate and unemployment rate across these periods. Perform this exercise

for a set of the largest metropolitan areas in the U.S.

The results are

displayed in the following figure.

Not surprisingly, we see that the unemployment rate in all these metropolitan areas went up since the recession began. However, the same is not true of job vacancy rates (that is, not all vacancy rates went down, as one might have expected). Specifically, while we observe the typical Beveridge curve dynamic in many jurisdictions (suggesting that cyclical factors are dominant), we also observe vacancy rates remaining relatively stable, or even rising, in several others (suggesting that structural factors are dominant).

So the tentative conclusion here is that the relative importance of cyclical vs. structural factors appears to vary across regions. To the extent that monetary policy is an effective stabilization tool, it cannot be expected to impact all regions of the country equally. In many regions, localized fiscal policies (education and training subsidies, etc.) may prove to be a more direct and effective tool.

Related story:

More Workers Moving for Out-of-State Jobs

Related story:

More Workers Moving for Out-of-State Jobs